In this week’s “Shipping Number of the Week” from BIMCO, chief shipping analyst, Niels Rasmussen, looks at the fact that despite a 70-80% fall in freight rates, and worsening of the supply/demand balance, liner operators have been able to keep rates higher than pre-pandemic levels.

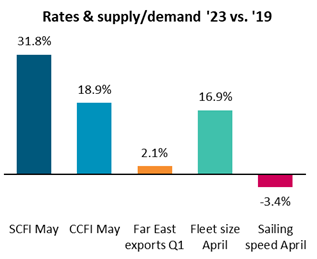

“The Shanghai Containerized Freight Index and the China Containerized Freight Index have dropped by respectively 81% and 72% since January last year. Yet, they remain higher than in 2019 despite a worsening supply/demand balance,” commented Niels Rasmussen.

Although export volumes from the Far East were relatively stronger in March 2023, first quarter volumes fell 8.5% year-on-year because of a market slowdown that began in the 2nd half of 2022.

As a result, the volumes were only 2.1% higher than during the first quarter of 2019. Exports to the three top regions, which account for 80% of volumes, were down 0.1% combined, with the Far East up 0.6%, Europe down 4.5%, and North America up 2.6%.

Except for the United States, Australia/New Zealand, and Lagos (Nigeria), the spot rates to all destination are, however, more than 10% higher in May 2023 than in May 2019. To the Mediterranean, Santos, Dubai, and Durban they are approximately double of what they were in May 2019.

During the last four years, the container fleet has grown 16.9% in size and ended April 2023 at 26.2 million TEUs, 3.8 million TEUs larger than in April 2019.

“The average sailing speed of container ships in April 2023 was 3.4% lower than in April 2019. This has limited the supply that the fleet can deliver. However, the total available fleet supply has still significantly outgrown Far East export volumes,” noted Rasmussen.

Despite this, the average spot rates for Shanghai exports (SCFI) and average rates for China exports (CCFI) remain significantly up vs. 2019. Recently, liner operators even appear to have been able to stem the freight rate slide and achieved some level of stability.

Idle ships currently add up to about 90,000 TEUs more than four years ago, but this cannot explain the higher rates or how liner operators have been able to stabilise freight rates.

Despite overall supply/demand developments, liner operators must have become more efficient at matching capacity to cargo demand and/or a newfound freight rate discipline has emerged with each liner operator.

“No matter the underlying reason, we can conclude that despite a 70-80% fall in freight rates, and a worsening of the supply/demand balance, liner operators have so far been quite successful in keeping rates higher than pre-pandemic levels,” said Rasmussen.