MDS Transmodal (MDST) and Global Shippers Forum (GSF) have concluded that current measures of competitiveness in the global liner shipping market are incomplete and therefore inaccurate and fail to take full account of the degree of cooperation between carriers which results in a more highly concentrated industry, to the serious detriment of shippers worldwide.

Thus, a modified measure is proposed, based on the alternative indicators suggested in a recent study produced by OECD/ITF and MDST, which according to a statement, better reflects the degree of cooperation by box lines, not just through the three big alliances (2M, THE, OCEAN) but also agreements under which lines in different Alliances operate shared services.

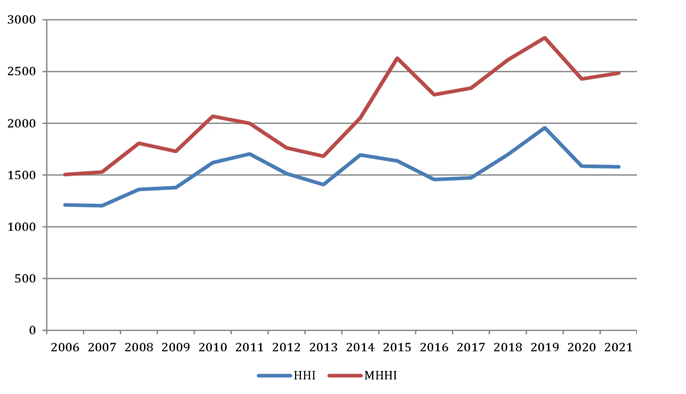

Competition authorities until now have relied on traditional but incomplete tools to assess the level of concentration across trades, most commonly the Herfindahl–Hirschman Index (HHI), according to GSF and MDST, which noted that “this indicator does not take into consideration the full extent of co-operation between shipping lines permitted under block exemption and other anti-trust immunity provisions.”

When these ‘inter-Alliance’ consortia are included in the concentration of the market, as measured by the modified HHI (MHHI), is much higher.

As an example, the following graph compares the traditional HHI of the Trans-Atlantic trade over the period 2006-2021, compared to an MHHI, which includes the inter-Alliance agreements on that trade. The Modified HHI exceeds the accepted threshold of 2,500 points at which an industry is considered ‘highly concentrated’, by most competition regulators.

On this basis, GSF believes the recent ‘Fact Finding Investigation 29 – Final Report’ published by the US Federal Maritime Commission (FMC) in May this year does not yet provide a complete picture, as the report maintains the liner trades serving the United States can be characterised as exhibiting “vigorous competition” because their HHI has been measured at below 2,500 points.

GSF urges the FMC and all other competition authorities to utilise the MHHI measure in its assessments of the container shipping market, and in particular of the concentration in market share achieved through all agreements permitted under block exemption and anti-trust immunity provisions.

“This breakthrough analysis lays bare the degree of dominance that many shipping lines actually have in the key global trades,” highlighted GSF’s director, James Hookham, who went on to say, “Current measures of market concentration are only seeing part of the picture. Not only are there consortia operations within the three main alliances, the number of separate consortia that exist consisting of lines from different Alliances is also significant.”

Hookham added, “Competition authorities should urgently revise their measures of competition to reflect the reality of the container shipping market and ensure they capture the full extent and effects of shipping line co-operation, as experienced by shippers”.

GSF believes that a lack of, or reduction in the levels of competition, leads to poor service quality for shippers. The forum noted that the number of port calls achieved (in comparison with those scheduled) fell to 68%, the lowest level recorded since this analysis began in 2020. Additionally, despite the fact that capacity lost through skipped ports in Europe declined in the first quarter of 2022, it continued to rise in Asia and Australia.

Mike Garratt, chairman of MDS Transmodal, concluded, “Several shipping consortia arrangements involve the constituent shipping lines controlling more than 30% of capacity in Asia to Europe market, in excess of the principle established in the European Union’s Consortium Block Exemption Regulation. Scheduled capacity between world regions has fallen and though our analysis indicates that service reliability has now stabilised the number of port calls skipped continues to grow.”